2025 RRSP contribution deductions and tax deferred income

The deadline to contribute to your Registered Retirement Savings Plan (RRSP) and claim a deduction on your 2025 personal income tax return is March 2, 2026. RRSP contributions reduce your taxable income in the year claimed, while investment earnings inside the plan accumulate on a tax-deferred basis. In practical terms, an RRSP provides two benefits: an immediate tax deduction and tax-deferred growth on investments held within the plan.

The deadline to contribute to your Registered Retirement Savings Plan (RRSP) and claim a deduction on your 2025 personal income tax return is March 2, 2026. RRSP contributions reduce your taxable income in the year claimed, while investment earnings inside the plan accumulate on a tax-deferred basis. In practical terms, an RRSP provides two benefits: an immediate tax deduction and tax-deferred growth on investments held within the plan.

Your deductible RRSP contribution is based on your available contribution room. For the 2025 tax year, the maximum contribution limit is the lesser of 18% of your prior year’s earned income (generally employment and self‑employment income) or $32,490, plus any unused contribution room carried forward from previous years. Your personal RRSP deduction limit is reported on your 2024 Notice of Assessment and can also be viewed through CRA My Account. It is important to confirm your available room before contributing, as excess contributions beyond your limit (other than the $2,000 lifetime buffer) may be subject to a 1% per month penalty tax until corrected.

If you are a Canadian resident, you are taxed on your worldwide income from your employment, self-employment - professional income, and income or taxable capital gains from any investments or property you may own. You are not taxed on gifts you receive and certain miscellaneous types of income. If your income is sourced in another country, you will normally receive a tax credit in Canada to avoid double taxation.

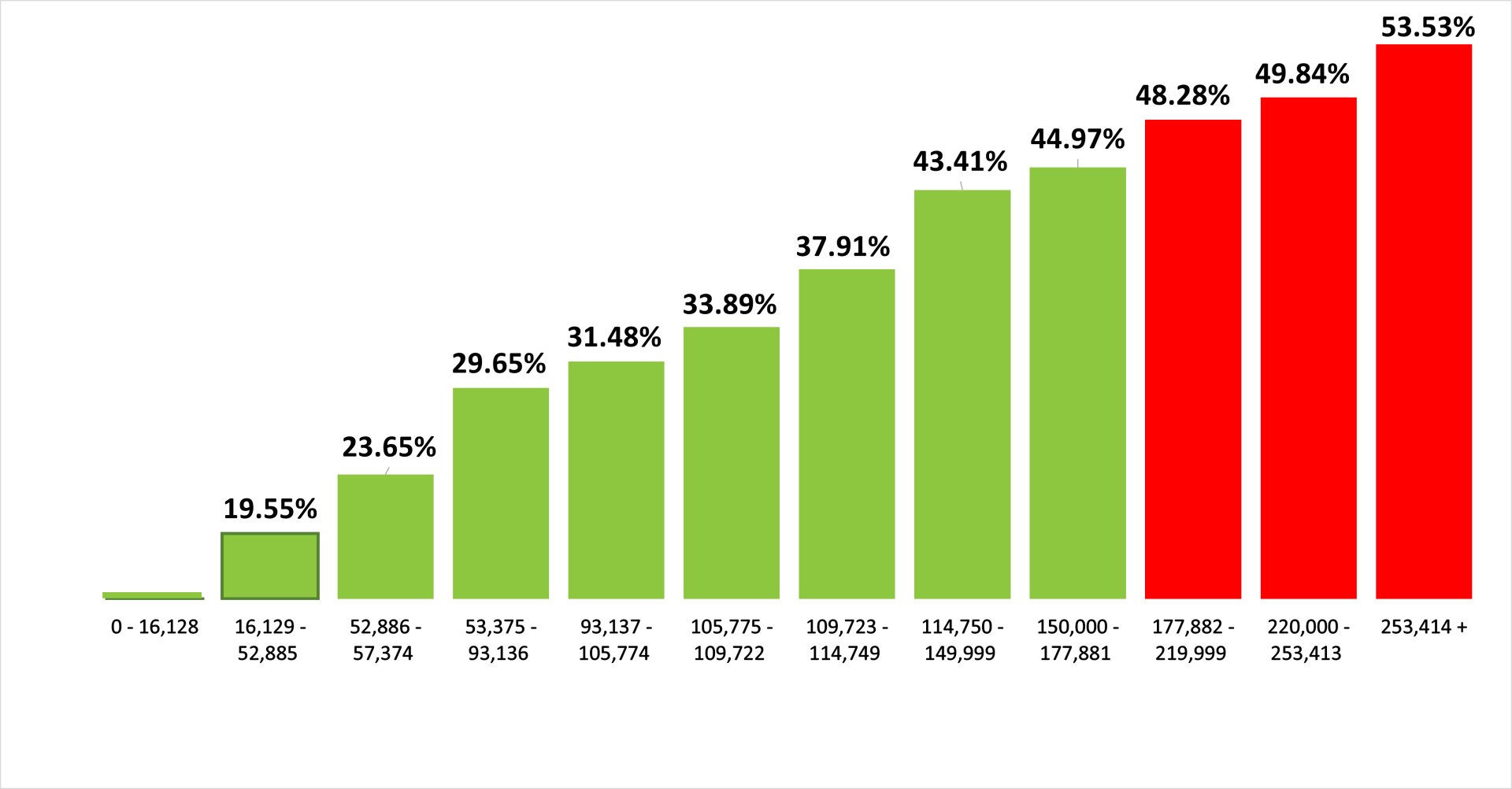

If you are a Canadian resident, you are taxed on your worldwide income from your employment, self-employment - professional income, and income or taxable capital gains from any investments or property you may own. You are not taxed on gifts you receive and certain miscellaneous types of income. If your income is sourced in another country, you will normally receive a tax credit in Canada to avoid double taxation. Canada’s income tax system levies federal and provincial taxes on individuals. Canada uses a progressive (graduated) income tax system where your earnings are taxed at higher rates (tax brackets) as your income increases. Tax brackets determine the rate of tax paid for each additional dollar of income within the defined bracket/threshold. Those with lesser incomes pay a lesser percentage of taxes on the income earned in lower tax brackets, while those earning higher incomes in higher tax brackets have to pay a higher rate of tax.

Canada’s income tax system levies federal and provincial taxes on individuals. Canada uses a progressive (graduated) income tax system where your earnings are taxed at higher rates (tax brackets) as your income increases. Tax brackets determine the rate of tax paid for each additional dollar of income within the defined bracket/threshold. Those with lesser incomes pay a lesser percentage of taxes on the income earned in lower tax brackets, while those earning higher incomes in higher tax brackets have to pay a higher rate of tax. A recent decision of the Tax Court of Canada provides important clarification for physicians and medical clinics operating under fee-sharing and cost-sharing models. In MedSleep Inc. v. The King (2025 TCC 70), the Court considered whether arrangements between a clinic and physicians resulted in taxable administrative services or exempt medical services for GST/HST purposes. The decision is particularly significant given the potential GST/HST cost exposure for physicians who provide exempt medical services and are not entitled to claim input tax credits.

A recent decision of the Tax Court of Canada provides important clarification for physicians and medical clinics operating under fee-sharing and cost-sharing models. In MedSleep Inc. v. The King (2025 TCC 70), the Court considered whether arrangements between a clinic and physicians resulted in taxable administrative services or exempt medical services for GST/HST purposes. The decision is particularly significant given the potential GST/HST cost exposure for physicians who provide exempt medical services and are not entitled to claim input tax credits.